National Student Money Survey 2025 – Results

The world of higher education is facing financial pressures across the board, and this survey uncovers the true impact the crisis is having on students' time at university.

Credit: Linda Bestwick – Shutterstock

Our thirteenth annual National Student Money Survey comes at a time of profound uncertainty in the university sector.

The 2025/26 academic year signals the first increase in tuition fees in almost a decade, and many fear that without further hikes, institutions could be forced to close. In the meantime, mergers are becoming more common.

But universities aren't alone in facing financial troubles. In the early 2020s, the Maintenance Loan in England suffered consecutive real-terms cuts. These have become baked into the system, despite warnings from ourselves and others that it would have dire consequences for students.

The findings in this report suggest that these fears are becoming realised. As was the case in our National Student Accommodation Survey earlier this year, many stats have seen little or no improvement since the height of the cost of living crisis. Instead, this level of hardship is becoming the new normal.

This is unacceptable, and we're repeating our calls for the government to increase Maintenance Loans to catch up with inflation, to ensure students receive the funding they need to thrive at university.

What's in our report?

- Key findings

- Students are struggling to get by financially

- How do students get money?

- How much money do parents give students?

- How much do students spend?

- Which areas have the highest student living costs?

- Food poverty at UK universities

- Do Student Loans stretch far enough?

- How would students get money in a cash crisis?

- Do students understand their loan agreements?

- Is university good value for money?

- How many consider dropping out due to money?

- What students expect from graduate life

Key findings from the National Student Money Survey 2025

These are among the headline findings from this year's National Student Money Survey:

- Surveyed students spend an average of £1,142 per month. Students in London spend the most at £1,269 per month.

- On average, the Maintenance Loan falls short of covering living costs by £502 per month.

- Over three in five (61%) skip meals at least some of the time to save money.

- Of those surveyed, 10% used a food bank in the 2024/25 academic year.

- The average parental contribution has dropped to £146 per month, with students from middle-income households the hardest hit.

- 41% have considered dropping out of university due to money-related issues.

Expert comment

Save the Student's student money expert, Tom Allingham, says:

This year's survey results confirm what we've long feared: that failing to tie Maintenance Loans to rising costs would lead to a never-ending cost of living crisis for students.

Although inflation has drastically fallen since its peak in 2022, the same cannot be said for the level of financial hardship uncovered by our reports. At £502 per month, the average shortfall between loans and living costs is close to its highest ever level, and more than three in five respondents are still skipping meals to save money.

At the same time, the average amount students receive from their parents is declining, with our findings suggesting those from middle-income households have been hardest hit.

Students from these backgrounds have always been at particular risk, as they're eligible for fewer bursaries, don't receive the maximum loan and, as these results show, come from families that often can't fund them to the extent expected by the government.

One simple solution is to raise the lower household income threshold – the point at which a student receives the maximum loan – to reflect the growth in average wages since it was set in 2007. This would drastically increase the amount most students receive, and in turn reduce the contributions expected from their families.

But first and foremost, Maintenance Loans must increase to catch up with inflation and reverse years of real-terms cuts. We're demanding the government do this, to ensure that funding a degree is no longer such a struggle for students and their families.

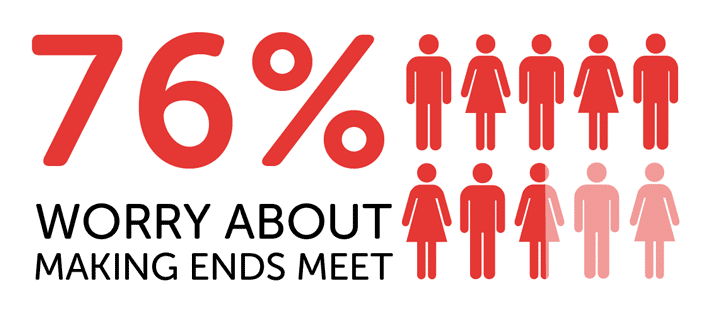

Students are struggling to get by financially

Having exceeded 80% for three consecutive years, the proportion of survey respondents worried about making ends meet (76%) has now dropped to its lowest level since 2021 (also 76%).

However, there is little to celebrate as, despite this small improvement, over three-quarters of respondents still cite it as a concern.

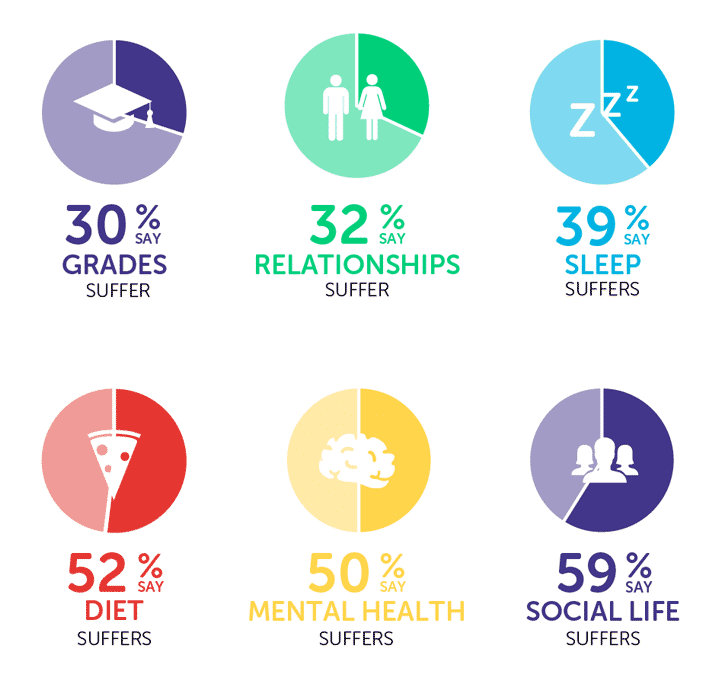

What's more, this stress doesn't exist in isolation. We asked students which other areas of their lives, if any, were impacted by money worries, and the vast majority (83%) said it affected at least one other aspect of their wellbeing.

This is a selection of quotes from respondents discussing the impact of financial struggles on their lives:

- I have five jobs around term time to manage finances and rent, so it's hard to do everything including meeting friends and uni work.

- I think and worry about money and budgeting every day.

- I feel like I'm in a good position because I live with my parents, but the thought of moving out scares me because I don't think I'd actually be able to afford to have a life and have a home.

- If I'm running low on money it means I can't afford public transport or petrol to travel to uni, meaning I missed a lot of uni in my first year.

- It [...] all feels too much, like I am underwater looking for how to stay afloat.

- [I] can't go out with friends because I have no money, which makes me feel lonely and a bit depressed. [It] stresses me out as well, which is not good for my mental health.

- Sometimes the thoughts go around in circles and ends up in a sleepless night [...] worrying about something I do not always have control over.

- I feel stressed that I can't go to many events or buy lots of new clothes like my friends do.

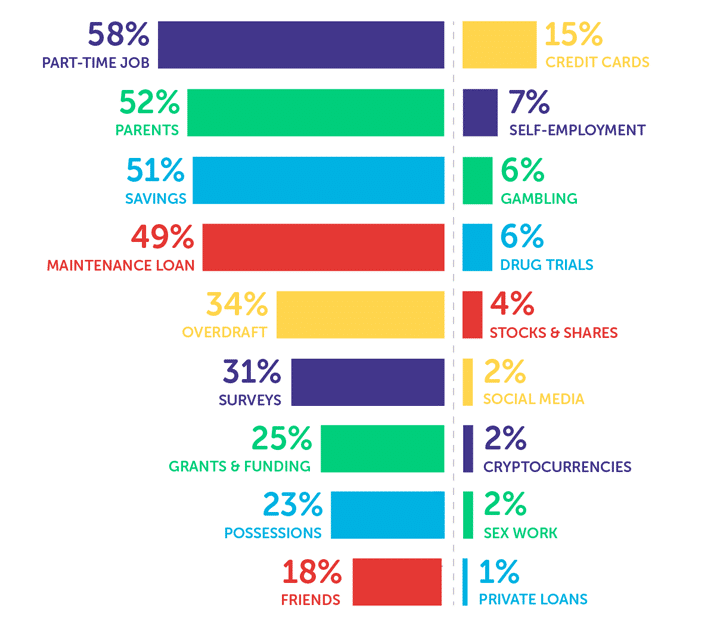

How do students get money?

These are the sources of money that surveyed students told us they use:

Just shy of three-fifths (58%) of respondents said they have a part-time job, while 52% receive money from their parents or guardians, and 51% draw on their savings.

Among the riskier or less conventional sources of cash reported were credit cards (15%), gambling (6%), drug trials (6%), stocks and shares (4%), cryptocurrencies (2%), sex work (2%) and private loans (1%).

Looking specifically at those who do paid work, the average amount earned was £547 per month. The average employed respondent worked an average of 36 hours per month, with 40% saying their studies suffered as a result.

10 surprising ways students have made money

Given the financial challenges they face, students are often forced to think creatively about how to boost their bank balances.

These are some of the most unusual ways respondents said they've made money:

- [I used to] collect and sell toilet roll and cardboard on eBay, it was desperate.

- [Getting] a 'fill a bag for £1' of books from the library, scanning them with WeBuyBooks and selling them.

- I helped someone on the train connect his bluetooth headphones to his phone and he gave me £20 to "get a coffee". I wasn't expecting anything in return but he was very sweet.

- Drinking out-of-date milk for a dare for £25.

- Selling a table which was left outside.

- Played games on my tablet to earn cash on Custard.

- Stood in line for someone from 3am – 8am to get a limited edition Pokémon card deck for £30.

- Writing erotica.

- Taking international children on tours of London.

- Buying and selling football shirts for profit.

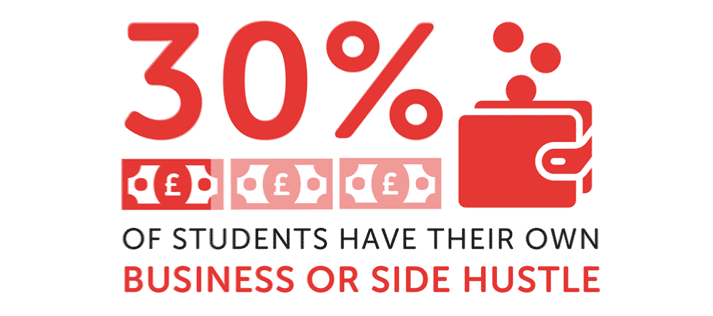

How many students have side hustles or small businesses?

As we found in 2024, 30% of respondents said they'd earned money from their own business or side hustle.

Although the vast majority had earned less than £500 in the past 12 months, there has been a year-on-year increase in those earning higher amounts.

| Earnings (past 12 months) | How many said they'd made this much (2024)? | How many said they'd made this much (2025)? |

|---|---|---|

| Less than £500 | 81% | 74% |

| £501 – £1,000 | 9% | 13% |

| £1,001 – £3,000 | 7% | 8% |

| £3,001 – £10,000 | 2% | 4% |

| £10,001+ | 1% | 2% |

Bursaries, grants and scholarships

A quarter of respondents (25%) said they'd received money in the form of a bursary, grant or scholarship.

That said, with 38% feeling they weren't made aware of funding in this form, it may be that some cash went unclaimed or that some students who would have been eligible didn't apply in time.

As we often stress, given the range of funds available – including some more unusual ones – it's always worth a student spending an hour or two searching for extra funding themselves, as it could make a huge difference to their financial resilience at university.

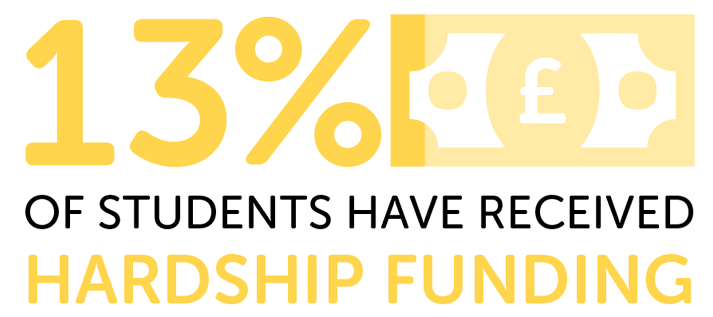

For those going through the most acute financial struggles, university hardship funding is an option.

Around one in eight (13%) respondents said they'd received this cash from their uni. This figure is slightly up on last year (11%), and the average amount received has also increased from £1,155 to £1,271.

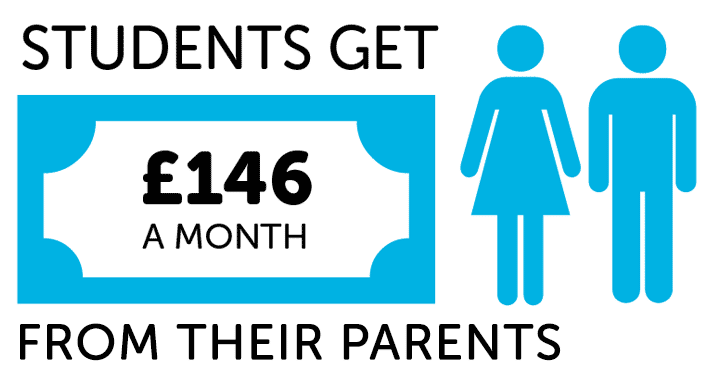

How much money do parents give their children at university?

Compared to 2024's results, there has been a notable decrease in the average parental contribution received by survey respondents.

In fact, at £146 per month, it's the lowest figure we've recorded since 2021.

But a more detailed look reveals that this drop hasn't been felt equally across the board.

Although the average contribution has indeed dropped among the lowest-income households, the decline is relatively small. And of course, depending on their exact household income and the part of the UK they're from, the government may expect no contribution at all.

Secondly, the average amount received by students in the two highest income bands has risen. This suggests that, as their children grapple with rising costs and a loan that falls increasingly short, parents are stepping in.

However, possibly the most notable takeaway is the huge drop in parental contributions among the other two income bands – the home of the 'middle-income student', a longstanding talking point in the sector.

| Household income* | Average monthly parental contribution (2024) | Average monthly parental contribution (2025) | Difference |

|---|---|---|---|

| £25,000 or less | £54 | £45 | - £7 |

| £25,001 – £35,000 | £102 | £93 | - £9 |

| £35,001 – £45,000 | £235 | £98 | - £137 |

| £45,001 – £55,000 | £246 | £157 | - £89 |

| £55,001 – £65,000 | £249 | £292 | + £43 |

| £65,001+ | £320 | £342 | + £22 |

*This only includes respondents who specified their household income. Students were presented with these six bands, as well as options for "Don't know" and "Rather not say", which some selected.

In very simple terms, those from the richest backgrounds receive the smallest loans because – in theory, at least – their parents can offer more support. At the other end of the scale, although students from the poorest backgrounds have little or no parental support to rely on, they receive the most funding from Student Finance and are eligible for more bursaries and grants.

In between these two groups are the middle-income students. They're eligible for far fewer income-based bursaries, and their parents often can't supplement their smaller loan to the extent expected by the government.

This problem appears to be getting worse, and there are two probable causes – the most obvious of which is the cost of living crisis, which continues to affect parents.

But less appreciated is the freezing of the lower income threshold (the point at which parents are expected to contribute) in England since 2007. This fiscal drag has led to fewer and fewer students receiving the maximum loan every year, and a real-terms decline in what all students are entitled to, relative to their household income.

This perfect storm leaves middle-income students facing difficulty making ends meet, and far fewer places to turn than their peers.

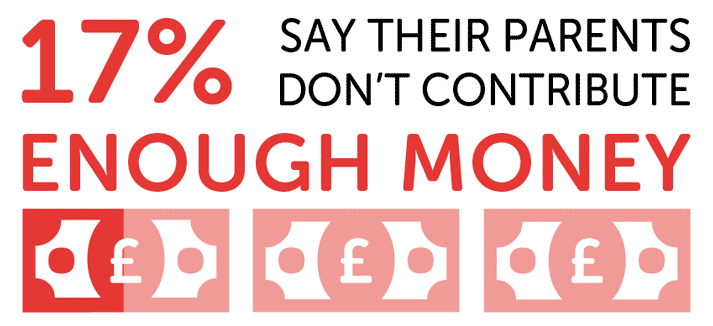

Despite all of this, just 17% of surveyed students said their parents don't contribute enough. However, it may be that respondents acknowledge the financial difficulties their families face and feel they can't ask for more.

Regardless, it seems clear that the lower household income band used by Student Finance England urgently needs updating to reflect almost two decades of inflation.

How much money do students have in savings?

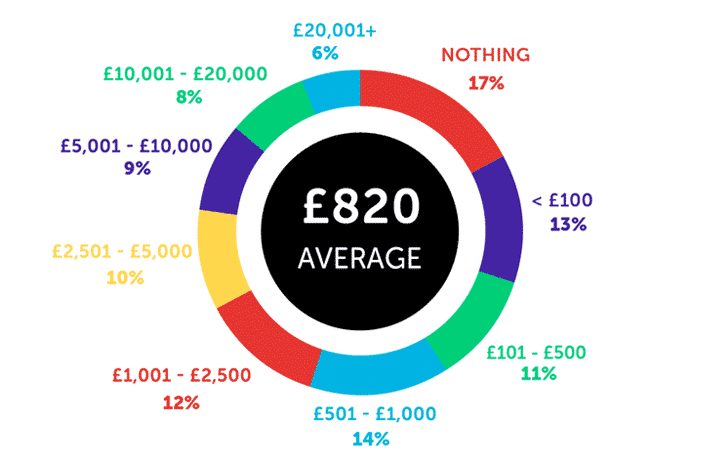

At the time of responding to the survey, 83% of respondents said they had at least some money in savings.

The average amount held was £820, although almost a third (30%) had less than £100.

Respondents reported a number of unusual or extreme ways in which they've saved money. Here's a selection:

- Bulk bought 120 packets of ramen for £100 so I could save money on groceries and takeout in the long run. Lasted me six months with a flatmate, so I'd say it worked quite well.

- Cooking everything in a dishwasher.

- Froze my bank card in a block of ice.

- Stayed [the] whole night in university toilets to save money on transport.

- Going to McDonald's for salt and condiments.

- I stored boiled water in a thermos every morning to save me paying to boil the kettle multiple times during the day.

- Setting timers for how long I could use water for in the shower (usually five minutes or so), and pausing it every time I turned the water off. If I ran out of time, I took the time out of my next shower. It saved me about £50 in utility bills.

- Taken unopened food out [of] the bin that my housemates have thrown away, which is still edible.

- Walk everywhere (even hours away).

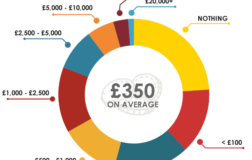

How much do students spend?

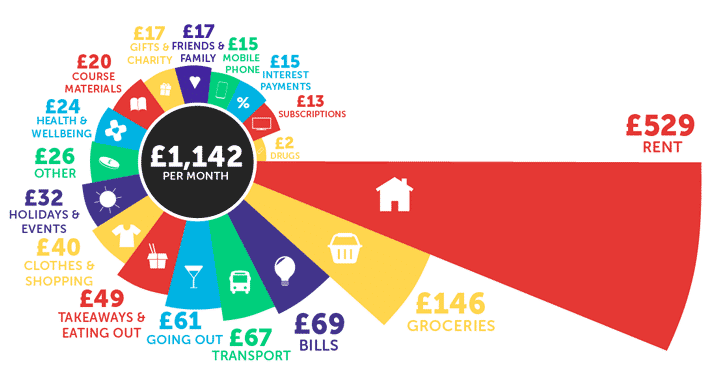

The average monthly spend reported by respondents was £1,142, with prices now rising at a more moderate pace than at the peak of the cost of living crisis.

Student spending has increased by around 3.4% compared to last year's average figure of £1,104 per month, which itself was up 2.4% on 2023. In the two years prior, we had discovered increases of 17% (2023) and 14% (2022).

Rent remains the single biggest expense for students, costing an average of £529 per month. Groceries are a clear second, with a monthly cost of £146.

But it's important to view these spending figures in the context of the survey's other findings, such as the significant proportion of students skipping meals to save money.

In other words, this level of spending is not what it costs to maintain what most people would describe as an acceptable standard of living. It's what it looks like when students are forced to cut back on even the most basic of essentials.

Student spending around the UK

These figures include all responses, including those from students living with their parents.

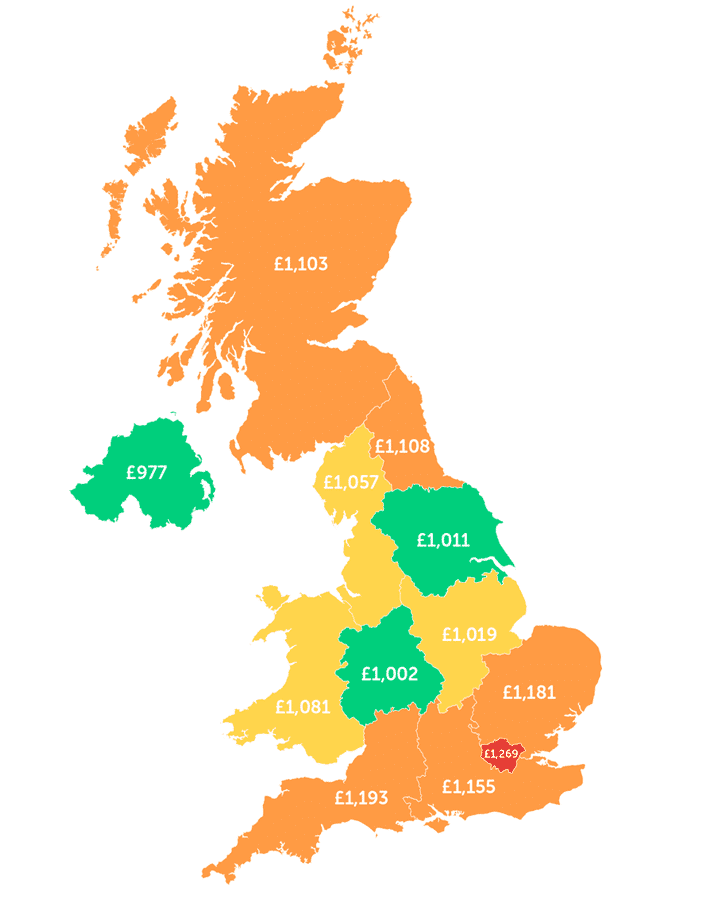

As ever, respondents in London reported spending the most on their living costs, averaging £1,269 per month.

Surveyed students in the neighbouring regions of the South East (£1,155 per month) and East Anglia (£1,181 per month) weren't far behind, although those in the South West (£1,193 per month) reported the second highest average overall.

The cheapest region, as it tends to be in our surveys, was Northern Ireland, with respondents spending an average of £977 per month.

Students are struggling with food poverty

The rising cost of food has accelerated this year, and ONS data (via The Food Foundation) shows that in the summer of 2025, it began to outpace overall inflation.

Our recent surveys have shown the cost of groceries to be a particular source of concern for students, and this year is no different.

The proportion of students telling us they'd used a food bank in the last academic year has risen slightly to 10% (up from 9%). Although this is a minimal increase – and significantly below the 2023 peak of 18% – it's still far too high a figure.

Fortunately, there has been a slight decrease in those saying they skip meals to save money.

This year, 39% said they sometimes skip meals, while an additional 22% reported doing so often. The total of 61% who say they do this at least some of the time is the lowest figure since we first asked this question in 2023, and down from last year's high of 67%.

Here is a selection of quotes from students in the survey discussing food banks and the cost of groceries:

- I come from a low-income family, and living at home we have all collectively had to use a food bank here and there.

- I keep wanting to cry when I think about food because I really wish I could afford to eat as much as my body is telling me to.

- I feel unworthy of food banks when there are kids that need it more.

- I have ADHD which affects my spending, and I'm lactose-intolerant so my food is more expensive.

- I have used all my four visits to food bank for the first six months, [I'm now] waiting to go again after six months.

- My uni has a free student food bank which I regularly use to top up between paydays.

- In first year, I could get my groceries [for] under £20 a week. Now I can hardly keep it under £35, and comparing receipts from then, I'm not the problem.

- I don't know much about [food banks] but it feels embarrassing to have considered it, so I would rather not use it. Friends have given me food before so that I have been able to eat.

Is Student Finance enough to live on?

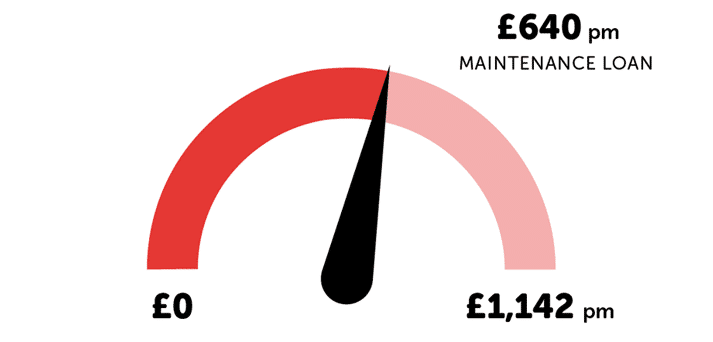

To help contextualise the findings of the National Student Money Survey, we always submit a Freedom of Information (FOI) request to the Student Loans Company (SLC) to uncover the average Maintenance Loan.

The SLC has confirmed to us that the average amount received by students from England in 2024/25 was £7,678 (£640 per month). However, with students spending an average of £1,142 per month on living costs, that still leaves a monthly shortfall of £502.

Compared to 2024's shortfall of £504 per month, it's clear – as we predicted in last year's survey, among others – that in the absence of an above-inflation increase to Maintenance Loans, this kind of financial struggle is becoming the new normal for students.

Go back just a few years to 2020's survey, and the shortfall was less than half its current level at £223 per month. This was far from ideal, but more easily bridgeable through parental contributions, part-time work and other funding.

Perhaps more than any other metric in any survey we conduct, the plateauing of the Maintenance Loan shortfall at around £500 per month underlines the extent to which students are at risk of a never-ending cost of living crisis.

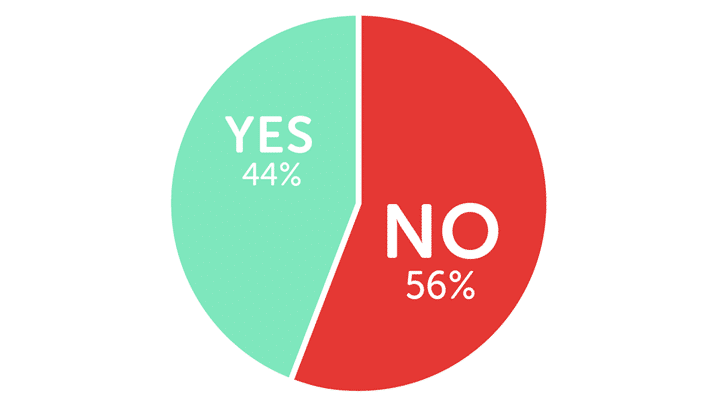

Despite this, only 56% of respondents felt the Maintenance Loan wasn't enough to live on, and just 54% believed Student Finance was unfair.

Here's what respondents had to say about the student funding system:

- I spent a lot of money on course costs, however my course is Makeup and the startup kit was £230. I'm sure students on other courses [...] only have to pay for their own stationery, which likely doesn't equal [...] £230. I think the Student Loan has to consider what sort of costs a student will have to pay, as this is significantly different depending on the course.

- I cannot take [out a] Maintenance Loan due to [the] interest on it. It is against my religion.

- We have to be grateful that we get money from the [government] in the first place. Parents are expected to contribute as well as part-time jobs, and I think that is completely fair.

- [You] should be able to take out whatever amount you want.

- They don't take into account the place we are living. I lived in Brighton, which [everybody] used to say had London prices, but didn't have London Student Finance to reflect that.

- My loan doesn't cover my rent, and not at all over summer. I get [the] minimum loan but my parents still can't afford to give me any money. This upcoming year will be the first they support me financially, because I was so upset they somehow found the money.

- Being a Nursing student is extremely difficult financially. This week alone, I've worked 52 hours and [was] only paid for 10, because that was the only day I worked at my job. The rest are unpaid placement hours.

- You can't live off £10,000 a year, especially as once rent comes out you're left with about a grand.

- [The system] punishes people who have [a] lower-income household by giving them more debt to pay back.

Do students have enough financial education?

The overwhelming majority of students in our survey (93%) said they budget – slightly less than in 2024 (94%). But the overall trend is one of increase compared to 2022 (85%), reflecting increased financial pressures.

However, the level of dissatisfaction with the financial education they've received suggests that, for many respondents, this may be something they're learning to do as they go.

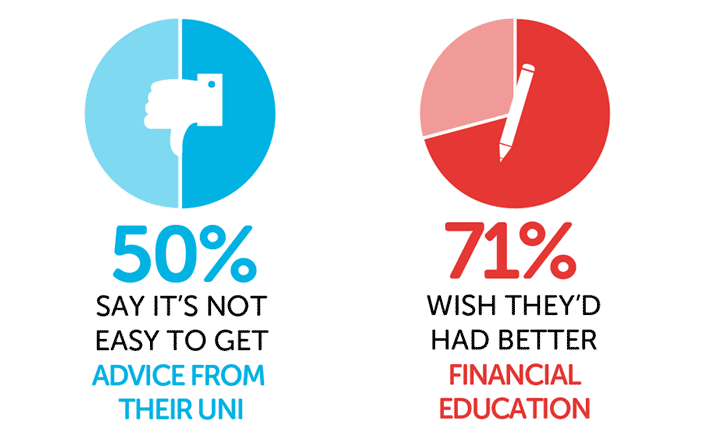

Almost three-quarters (71%) said they wish they'd had better financial education in school – a figure that has seen very little change in the long term.

| Survey year | How many wish they'd had better financial education? |

|---|---|

| 2020 | 71% |

| 2021 | 74% |

| 2022 | 74% |

| 2023 | 64% |

| 2024 | 74% |

| 2025 | 71% |

Financial education has been part of the English secondary school curriculum since 2014, yet clearly much more needs to be done, particularly if Maintenance Loans are to remain so inadequate.

By contrast, the data suggests that universities have become much better at providing financial support and advice – or, at the very least, at signposting it.

Of those who have tried to access help from their uni, 50% said it wasn't easy. There's still a long way to go, but this is the lowest figure we've ever recorded for this question (and down from 56% in 2024).

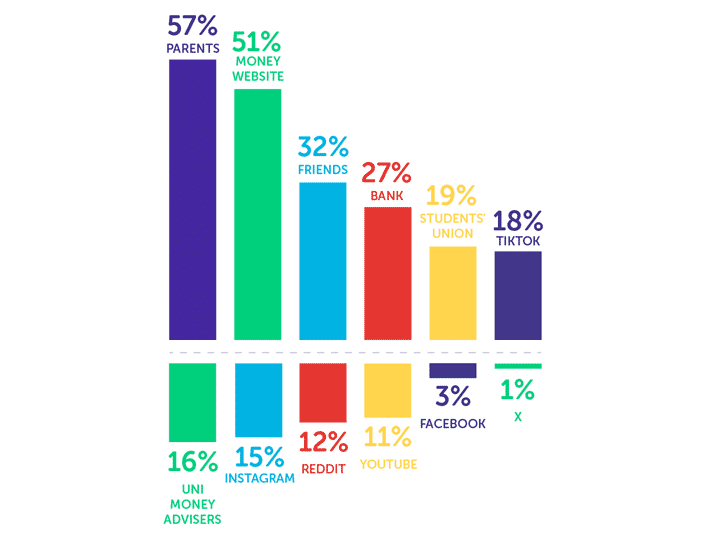

Despite the apparent improvements from universities, they remain among the least common places respondents turn to for financial guidance (15%, with 19% going to their students' union). Parents are the most popular source of advice (57%), with money websites a close second (51%).

A combined 42% said they use at least one social media website (TikTok, Instagram, Reddit, YouTube, Facebook or X/Twitter) as a source of financial guidance.

While these platforms can be an effective way to share money advice – indeed, Save the Student has a presence on all of them – it's also true that they can be a hotbed for misinformation.

It's vital that students are cautious when seeking advice on these platforms, and look to either verify the information elsewhere or check how trustworthy the source is.

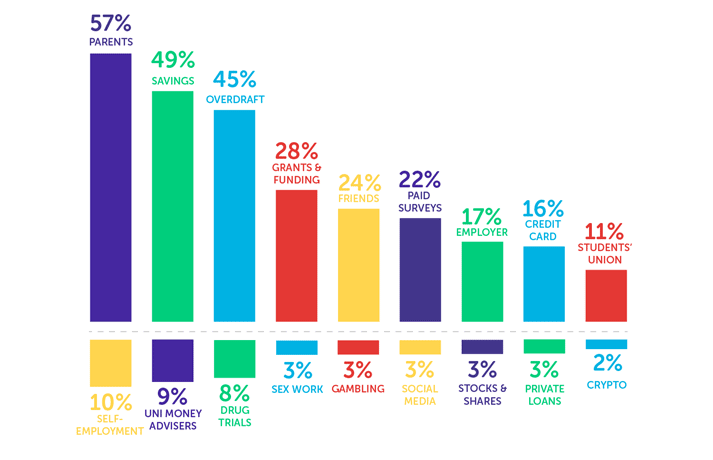

How would students get money in a cash crisis?

With students facing enduring financial hardship, we asked respondents where they would go for money in the event of a cash crisis.

As has always been the case in our surveys, parents remain the most common source of emergency cash – and this year, 57% said that's where they'd turn to. Savings (49%) and overdrafts (45%) were the next most common, indicating a safety-first approach even in times of crisis.

Looking specifically at the less common answers, it's striking that the proportion saying they would turn to each form of income is remarkably similar to those who already do – often within one or two percentage points.

In previous surveys, there tended to be a marked increase in the numbers saying they would turn to the likes of sex work or drug trials in a cash crisis, compared to in normal times. The narrowing of this margin suggests that, in at least some cases, students feel they're already in an emergency and are exhausting all options.

Here is a selection of comments from surveyed students who have used, or considered using, sex work as a source of cash:

- I only do this when I'm really desperate, as I really don't enjoy it.

- It is a morally taxing thing to do, especially when it doesn't pay well.

- Me and my friends have written erotica, worked as dominatrixes and sold used knickers to make up the money for rent.

- To be honest, when I was at my lowest and didn't have any money, I did think about doing OnlyFans, but I was not comfortable in the end.

- Was for fun mostly, only lasted a few months.

- It's just my feet, I'd probably feel uncomfortable if I turned to other forms of sex work.

- I have often thought about turning to this sort of work solely so I could survive. I have parents I wish I was estranged from, however I can't cut contact and endure verbal abuse because it's better than being homeless. If I cut them off, this type of work may be the only thing I [could] do to keep a roof over my own head.

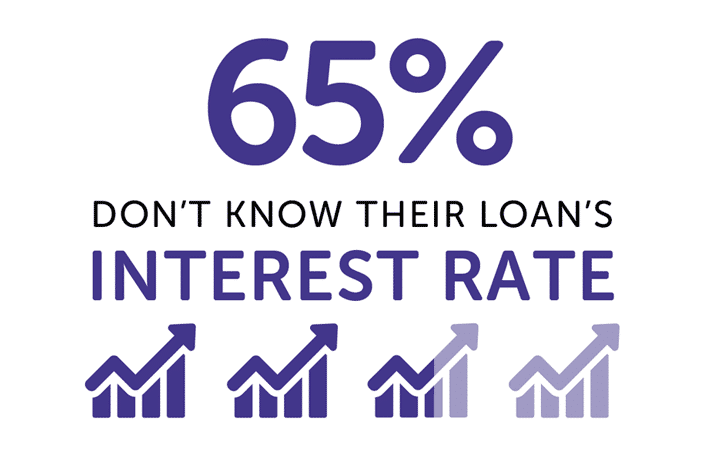

Do students understand their Student Loans?

The majority of respondents reported being unsure about at least one aspect of their loan agreement.

Approximately two-thirds (65%) said they didn't know their loan's interest rate (down from 72% in 2024). And with four different repayment plans using three different mechanisms for determining the interest, it's perhaps understandable that large swathes of students don't know every detail.

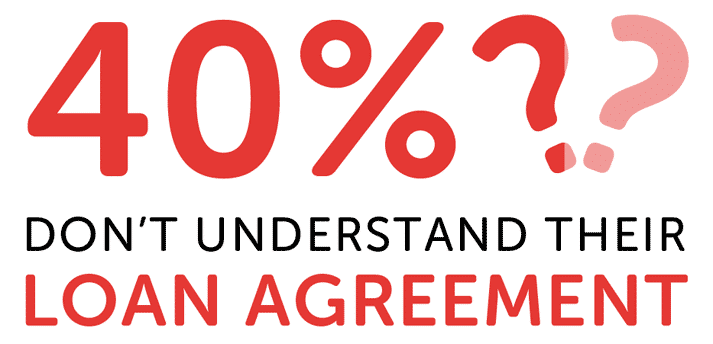

Four in five respondents told us they didn't understand the terms of their loan agreement in full (down from 45% last year).

Again, the fact that current students could be on one of four repayment plans has likely not helped, particularly as the discourse tends to focus on whatever the current arrangement is in England.

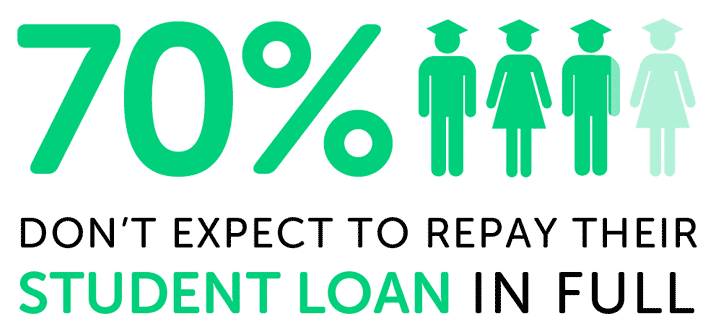

Seven in 10 said they don't expect to repay their loan in full, although 9% weren't aware that any remaining balance is wiped at the end of the repayment term.

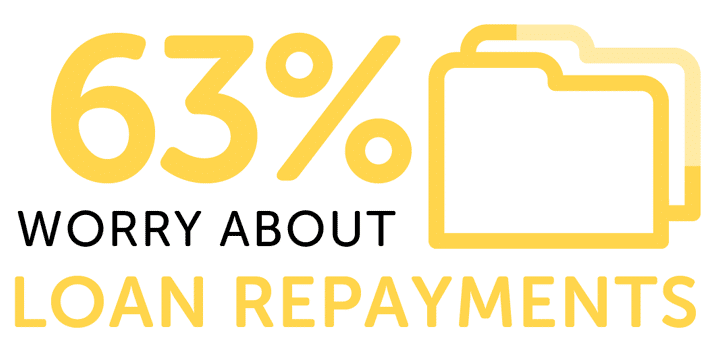

And finally, 63% of respondents said they were worried about their Student Loan repayments (down from 70% in 2024).

While any salary deduction is unwelcome during a cost of living crisis, we always like to emphasise that Student Loan repayments should be manageable for most graduates.

Even with Plan 5's increased monthly payments and longer repayment term, deductions remain tied to a graduate's earnings and are paused if their salary drops below the threshold.

Students should be reminded that, in many ways, their loan repayments will operate slightly more like a tax. If they earn more, they pay more. If they earn less, they'll pay less or nothing at all.

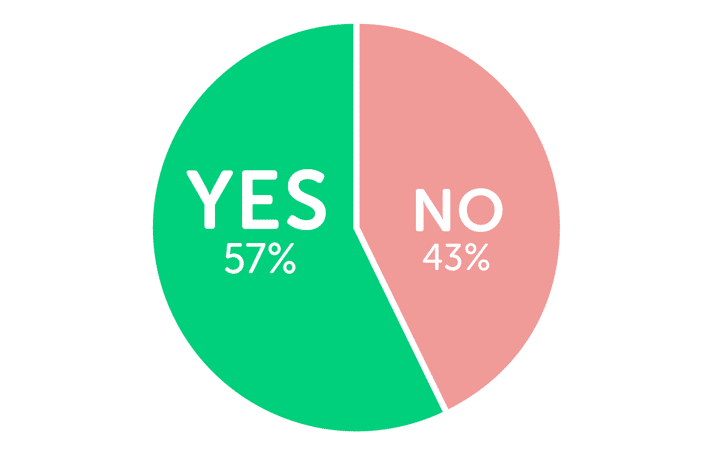

Is university good value for money?

Despite an impending tuition fee hike and a lack of maintenance funding, over half of the respondents in our survey felt that their university experience represented good value for money. In fact, at 57%, this is higher than in 2024 (54%).

Although the government has remained tight-lipped about any future hikes, there is a feeling that tuition fees will inevitably increase again in 2026/27. Universities are facing their own financial difficulties and, without this additional income, it's feared some institutions could collapse altogether.

That said, we don't believe this additional funding should come from students, and are instead calling on the government to increase grants.

This is what surveyed students had to say about tuition fees in the UK:

- Once tuition fees are scrapped it will be fair again.

- Paying around £9,000 a year is a lot. But then having to pay interest on top of that is impossible and makes me feel scared [about being in] student debt after I finish university.

- I believe higher education should be accessible to everyone, regardless of financial background. Lowering or removing tuition fees would reduce the long-term debt burden on students, while lowering interest rates on Student Loans would make repayments more manageable.

- I think uni shouldn't be so expensive, considering we only have about six to eight hours of lectures per week and they can be done online. I find it ridiculous this costs over £9,000 per year, and we're only at uni each year for eight months!

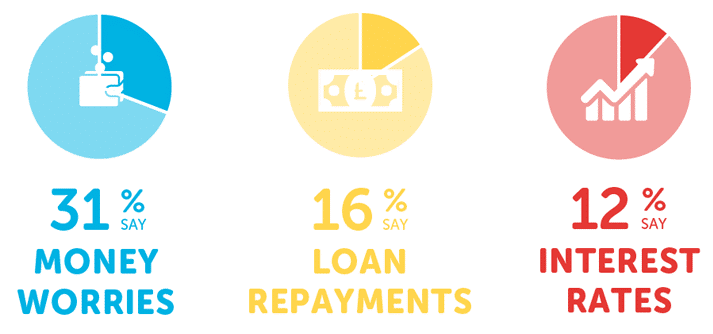

How many students think about dropping out due to money?

In the absence of official data on the reasons for students dropping out of university, we asked our survey respondents if they had considered leaving their studies for any one of three money-related reasons.

Just under a third (31%) had thought about dropping out due to money struggles. The size of Student Loan repayments was a factor for 16% of respondents, and 12% cited Student Loan interest rates. Each of these figures is lower than in 2024 (38%, 17% and 18% respectively).

Around three in five (59%) said they hadn't considered dropping out at all.

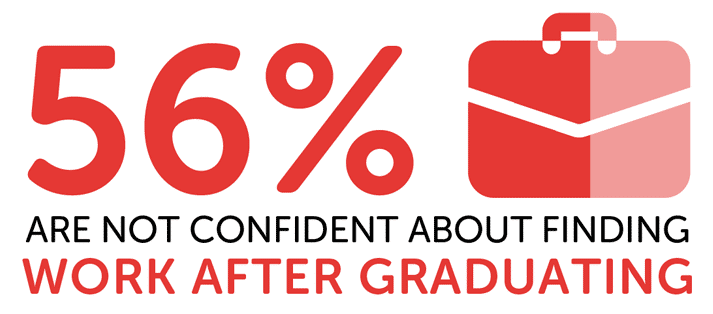

What students expect from graduate life

Recent reports have suggested that graduates are facing a difficult job market, and that seems to be reflected in the mood of our respondents.

Over half (56%) said they weren't confident of finding work after graduating, representing an increase of four percentage points on 2024 (52%).

| Survey year | How many weren't confident they'd find a job after uni? |

|---|---|

| 2020 | 58% |

| 2021 | 62% |

| 2022 | 45% |

| 2023 | 42% |

| 2024 | 52% |

| 2025 | 56% |

Following a post-COVID rise in optimism, it seems respondents are once again becoming nervous about their graduate job prospects. The growth of AI, as well as perceptions of a stagnant economy, are likely to be factors in their thinking.

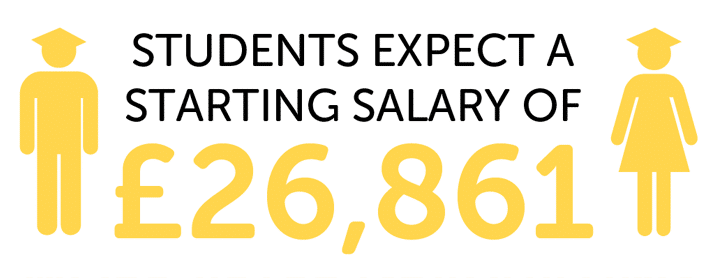

Nonetheless, there has been a notable increase in the expected starting salary. On average, surveyed students told us they expected to start their first job on £26,861, an increase of 7.2% on 2024 (£25,058).

There is, however, a significant gender split in the responses.

Those identifying as male expected an average starting salary of £29,152, while respondents identifying as female anticipated earning just £26,040. Respondents who identify in any other way, or who preferred not to say, expected a starting salary of £20,000.

When split by household income, there's also a broadly positive correlation between household income and expected starting salary as a graduate.

| Household income* | Expected starting salary |

|---|---|

| Less than £25,000 | £25,366 |

| £25,001 – £35,000 | £26,379 |

| £35,001 – £45,000 | £24,814 |

| £45,001 – £55,000 | £27,238 |

| £55,001 – £65,000 | £30,241 |

| £65,001 or more | £30,575 |

*This only includes respondents who specified their household income. Students were presented with these six bands, as well as options for "Don't know" and "Rather not say", which some selected.

What others say about the survey

In response to the survey, Skills Minister Jacqui Smith said:

University should be a time to grow, thrive and prepare for your future career, but this government recognises that too many students are facing real financial hardship.

That's why I am determined to fix the foundations of Higher Education to deliver change for students – restoring universities as engines of growth, aspiration and opportunity.

Our Post-16 Skills Strategy White Paper will soon set out how we plan to improve access for students from disadvantaged backgrounds, and ensure universities are delivering world-class teaching and clear routes into good jobs.

Vivienne Stern MBE, Chief Executive of Universities UK (UUK), said:

Money should not be a barrier to students accessing life-changing opportunities at university or be a reason students consider dropping out. Universities are stepping up efforts, with many offering bursaries, support schemes and assistance funds, but they can only do so much, particularly in the current financial climate.

We also need governments across the UK to increase the student maintenance package, and we were pleased to see the Maintenance Loan in England increase in line with inflation this year. Moving forward, we believe this should be a permanent policy, so that students are not faced with falling support at the same time as costs rise.

For any student that is struggling, we would encourage you to talk to your university's student support team.

About this survey

Save the Student has been running the National Student Money Survey since 2013. Our independent findings provide insights into the realities of student money and inform the content on this website.

The survey was conducted entirely online.

We push it out to a mix of our own followers, distribution via student service centres and unions at some universities, as well as through social media promotion. This mix is done to ensure that we are not only polling our own users.

Figures have been rounded to the nearest whole number.

For more information about this survey, case studies or expert comments, please get in contact.

- Source: National Student Money Survey 2025 / www.savethestudent.org

- The average Maintenance Loan amount is based on FOI information from the Student Loans Company (SLC).

- The survey received 1,151 responses.

- Students were polled between June and August 2025.

- Data from our previous surveys.

- Save the Student's Press Page.

- Tools and resources.

Student Money Cheatsheet

In response to recent survey findings, we have created the free Student Money Takeaway resource for university students.

This is a printable PDF, and it includes a one-minute budget sheet. In the resource, you can find the best advice from our website condensed down to a couple of pages.

![What do students spend money on? [stats]](https://www.savethestudent.org/uploads/what_students_spend_money_on2-252x160.png)

![What do students spend money on? [stats]](https://www.savethestudent.org/uploads/what_students_spend_money_on2-100x100.png)