Banking terms explained

With more technical terms than a physics textbook, the world of banking can be difficult to navigate. Use this guide to brush up on your banking terminology and be fazed no more.

Credit: Vladimir Sukhachev – Shutterstock

The older you get, the more you think it – maths lessons at school should really teach you about banking.

One day, you're at school, with mum and dad taking care of all things money-related. The next you're at uni, and all of a sudden you're expected to manage your finances despite never having been taught about any of it.

If you're unsure of the lingo, dealing with banks and money can be a little trickier than necessary. Use this page as your go-to guide for all the banking jargon you might need as a student.

What's in this guide?

Basic financial terms explained

Before we dive into the really meaty stuff, let's check that we know what the basic banking terms in the UK mean. We'll be using some of these later on to describe the more complicated phrases, so it's worth making sure that you've got a good grounding.

What is a current account?

A current account is a one-stop shop for managing your day-to-day finances. Most people will just refer to it as their bank account, and it's usually where your Maintenance Loan or salary will go.

As a student, you'll most likely have a student account (and a graduate account once you've left uni), but these are just different types of current accounts.

What is interest?

Interest is the charge you pay for borrowing money. It is usually charged as a percentage (otherwise known as the interest rate) of the sum of money you may have borrowed and will be added on over time.

When you borrow money from a lender, there's a good chance that you will have to repay it with interest. You can effectively think of it as a way to thank the lender for giving you the money and allowing you to repay it in instalments.

Similarly, when you put your money into a savings account, you'll gain interest on top of it. This time, the tables have turned, and you can see this as the bank's way of saying 'thank you' for using their services.

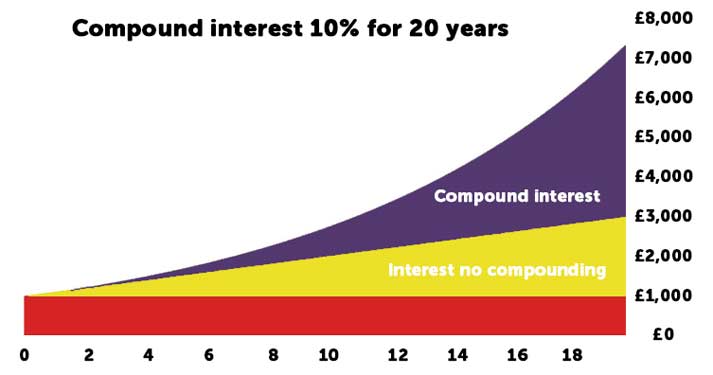

What is compound interest?

Whether you're borrowing or saving, you'll probably come across the phrase 'compound interest'. As opposed to normal interest (which is just based on a percentage of the original sum of money), compound interest also accounts for the money added on by previous instalments of interest.

Compound interest is probably best explained using an example, so let's give it a crack.

Imagine you had £1,000 and added 5% interest – you'd now have £1,050.

Fast forward to the next time interest is added, and rather than just gaining 5% on the original amount of £1,000 (£50), you'll also be earning 5% on the £50 of interest added last time (£2.50). This means that the amount of interest added will increase with each instalment.

In a nutshell, this is the principle of compound interest: adding a percentage of a percentage.

If you've found compound interest really... well, interesting, find out more in our list of money lessons that you should have been taught at school.

What is an overdraft?

An overdraft is like a buffer attached to your current account, giving you some money just in case you ever use up all of your own.

You may be charged a fee or interest (or both) by your bank for entering your overdraft. It's therefore important that you keep on top of your finances and don't go too far into your overdraft.

Student bank accounts often come with an interest-free overdraft, which (as the name suggests) allows you to use a certain amount of your overdraft without paying interest. The overdraft may also be fee-free, meaning you won't be charged for using it.

The final key aspect of overdrafts is that they can be split into two sections:

- Planned overdrafts – These are also known as arranged overdrafts, and they refer to ones that you've agreed with your bank. When confirming this with them, you'll also agree on any interest rates or fees attached to your planned overdraft.

- Unplanned overdrafts – Unplanned, or unarranged, overdrafts come into play when you exceed your planned overdraft allowance. At this point, you're likely to be charged much higher interest rates and fees, so avoid it if possible.

If you've got any more questions about overdrafts, or you're after some tips on how to use them safely, read our guide to overdrafts.

What is credit?

Credit: Ink Drop – Shutterstock

Credit is a phrase that's used in conjunction with lots of other words (like credit card or credit rating), but it can be used by itself in one of two ways:

- To be 'in credit' means that you have more than £0 in a given account. You'll see this on your current account if you're not overdrawn, or on a bill if you've accidentally overpaid (meaning that your account with that company is in credit because it has more money in it than needed).

- To 'have credit' means that you've borrowed money from a lender.

What is debit?

To be 'in debit' means that you owe money. Again, you might see this on a bill if you've not paid it yet. They could describe your account as being in debit to the value of £70, meaning that you need to pay them £70.

What's the difference between credit and debit cards?

A credit card is essentially an agreed way of borrowing money on a consistent basis. That's not to say you don't have your own money to spend – it just means that you're delaying the point at which you're using your money.

Sadly, you will have to pay back the money you've spent on a credit card, with interest often added on too.

If you ever want to get rid of a credit card, you can cancel it fairly easily. But remember, you'll need to pay off any outstanding debt on the card before you're completely shot of it!

A debit card is a card that gives you access to the money in your current account. When you use a debit card, you're either spending your money or dipping into your overdraft.

More complex financial terms explained

Right, we've covered the basics. Now let's look at some slightly more complex terms.

What is a Direct Debit?

If you've ever been responsible for paying for your own phone contract, you'll have probably paid via Direct Debit. In fact, most regular bills can be paid in this way.

Setting up a Direct Debit means that you've told your bank to pay money to a certain organisation on a regular basis (often on a specific day each month). The amount may be the same each time, but it can change when appropriate (we've all had to pay the price for exceeding our data allowance).

Direct Debits are controlled by the organisation that you're paying the money to. They set it up, and they control how much and how often you pay them. This is just one of the many reasons to regularly check your bank statement, just to make sure you've not been overcharged.

Although Direct Debits are controlled by the organisation being paid, you can cancel them at any time – but don't expect the company to keep providing a service if you stop giving them money.

What is a standing order?

Standing orders are very similar to Direct Debits, but with a couple of key differences. Firstly, unlike Direct Debits (which are controlled by the recipient), a standing order is controlled by you. You set it up, and you control how much and how regularly the payments are made.

The other important difference is that a standing order will always be for the same amount of money. You can elect to change the amount, but this will be a permanent change – if you want to transfer a different figure each month, a standing order probably isn't for you.

Rent payments are a perfect example of when a standing order should be used. Rent is usually paid in equal instalments every week or month, and usually on the same day.

By setting up a standing order, you can make sure that your rent gets paid without having to remember to do it (although you will have to make sure there is enough money in your account!).

What is a credit score?

Put simply, your credit score (also referred to as a 'credit rating') decides how generous a lender will be when they give you money.

It will affect how much they lend you (if at all) as well as how much interest you'll pay, so it's super important to try and keep your credit score as healthy as possible.

What is a guarantor?

When you borrow money from a lender or sign a contract to make regular payments (like when you agree to rent a property), you'll usually be asked to provide a guarantor.

A guarantor is essentially your safety net. They are expected to make payments for you when you can't, so they will need to be financially secure themselves – or at the very least, have a good credit score.

Try to think of a guarantor as a kind of insurance: hopefully, you'll never need them, but everyone's happier knowing that they're there just in case.

What is an ISA?

Acronyms are everywhere in finance, and this is one of the biggies. An ISA (Individual Savings Account) is a savings account that allows you to store money without having to pay tax on the interest gained.

The tax-free nature of ISAs is why they were historically a very popular way to save larger sums of money. However, in 2016, the law changed to allow a significant proportion of the population to save money in a normal savings account without paying tax on the interest.

If you haven't already, we recommend looking into getting a Lifetime ISA (LISA) – you can get a 25% bonus on your savings from the government, up to £1,000 a year.

The most complicated financial terms explained

Ok, we'll admit it – these aren't the most complicated financial terms out there. But they are the most complicated ones that you'll need to worry about as a student.

Before we start, just as a warning, we'll be looking at AER, APR and EAR. These all look pretty similar – they're all acronyms, and they've all got an A and an R in them.

What's more, they are pretty similar. But they do refer to different things, so it's worth getting your head around what they mean.

Right, if you think you're ready, let's delve into these bad boys.

What are fixed and variable interest rates?

When you borrow or save money, you'll be told whether or not it's subject to a fixed- or variable-rate interest. Here's a quick overview of what these terms mean:

- Fixed-rate interest – These rates don't change for the duration of the agreement, which could be the repayment period or the time in which you keep your money in a savings account.

- Variable-rate interest – This means that the interest rate can (and probably will) change over time, often in line with measures of inflation, like RPI (Retail Price Index).

As our guide to Student Loan repayments explains, interest on your Student Loan accumulates at a variable rate according to the rate of RPI.

What is RPI?

RPI stands for Retail Price Index and is a measure of inflation. Ultimately, it tracks changes in the price of a set 'basket' of items that consumers regularly buy.

Some things, like milk and bread, will always be in the 'basket', whereas other things, like gin, will come and go based on popularity. Over time, the changes in the prices of the items in the 'basket' are used to determine the rate at which inflation is occurring.

Ordinarily, you wouldn't need to worry too much about RPI – but as we said above, your Student Loan accumulates interest at a rate that can be influenced by RPI.

What is AER?

AER stands for Annual Equivalent Rate – the official rate of interest for a savings account. This represents how much interest would be paid over the course of a year, and allows for an easy comparison between multiple accounts (particularly as different accounts may pay interest at varying intervals).

Interest on a savings account may also be advertised as a gross rate. The specific differences between gross and AER aren't really worth understanding, but the gist is that AER takes into account compound interest, whereas gross doesn't.

When the interest on an account is paid annually, the gross rate and AER should be the same, because there's no compound interest. If the interest is paid monthly, AER will be slightly higher than the gross rate as it accounts for the interest gained on the existing interest (e.g. 5% gained on the initial amount, plus 5% on the 5% that was gained last month).

The only thing you need to remember is that you should never compare AER with gross rates. AER and gross rates are different things, so you should only ever compare AER with AER, and gross with gross.

What is APR?

Credit: Chermen Otaraev – Shutterstock

APR stands for Annual Percentage Rate. This refers to the official rate at which you've borrowed money, including any associated fees, essentially giving a complete picture of how much the debt will cost.

Remember that APR does not necessarily equal the interest rate, as it also includes fees. For example, if you borrowed money at 11% APR, you could have an interest rate of 9%, plus additional charges which are the equivalent of an extra 2%.

This seems complicated, but it allows a fair comparison between lenders (otherwise they could advertise a low-interest rate, but chuck loads of additional fees on top to make it more expensive than another loan with higher interest rates).

You’ve probably heard ‘representative APR’ being blurted out at high speed by the voiceover on an advert for loans. This is just a guide based on the fact that at least 51% of successful applicants will get the advertised rate, while the other (at most) 49% of people could get a higher rate.

It’s also important to understand that you might never pay the advertised APR.

Lenders will often try to entice you by offering a lower APR for a certain amount of time at the beginning of the repayment period (let’s call this APR1). After this (usually very short) time has passed, the APR will increase (to what we’ll call APR2) for the remainder of your repayments.

As you’ll have two different types of APR throughout your borrowing period, the lender will advertise what is essentially an average figure for what the APR will be until you’ve paid the money back. Since you’re likely to have APR1 for a much shorter time than APR2, the average APR will be much closer to APR2.

In simple terms, the advertised APR can sometimes just be the average APR, with the majority of your repayment period being at a slightly higher rate. Again, while this seems complicated, it does make it easier to calculate and compare the overall cost of borrowing!

What is EAR?

Last but not least, we have EAR – Effective Annual Rate.

EAR is actually very similar to APR, but while APR is only used to refer to products that exclusively lend money (such as a loan or a mortgage), EAR applies when you’re talking about a product that can also be in credit (such as a current account).

You’re most likely to see EAR being used to describe the interest on an overdraft. EAR is calculated using three factors: the interest charged if you’re overdrawn, how often interest is charged, and what the effect of compound interest is on your debt.

Again, if you dive too deep into this, you can get lost. All you really need to remember about EAR is what it refers to, what it’s formed of, and that it doesn’t include overdraft fees.

Keen to learn more about your finances? Have a read of our guide that debunks the big Student Finance myths.